Thadeus Geodfrey is an experienced and celebrated writer and self-taught trader specialising in cryptocurrencies and forex. Market analysis, identifying fraudulent brokers, and security are his cup of tea. At BrokerRaters Thadeus develops educational materials and user guides, offers market insights, and ensures our content conforms to the best standards. Join Thadeus to succeed in your trading endeavors.

Fact checked

Advertising Disclosure

We may receive compensation from our partners for placement of their products or services, which helps to maintain our site. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn’t influence our assessment of those products.

Are you a Brit aged 18-29? If you are, and you’d like to save for your first home or your sunset years, we highly recommend opening a Lifetime ISA. With this account, you can save money and earn a 25% government bonus on your contributions. But to reach your financial goals, mitigate risk exposure, and ultimately have access to a juicy nest egg, you must save with the right provider.

We understand how complicated and hectic finding the best Lifetime ISA in the UK provider can be when so many options are available. To make this task easier and save you precious time, our experts have vetted the institutions that offer Lifetime ISAs in the UK and recommended the best in this guide.

We’ve recommended 5 providers in the UK. Your job is to pick one; remember, although you can have multiple LISAs, it’s pointless since you are limited to paying into only one each year.

While selecting a Lifetime ISA provider, consider important factors like licensing, minimum deposit requirements, and annual interest rates. Below’s a quick rundown of where the best Lifetime ISA providers in the UK stand based on these elements. Please note that the numbers we’ve included below are exclusively for Lifetime ISAs.

To successfully save for retirement or your first home, you need a LISA provider with the right products. That is important since numerous options are available today, including cash and stocks & shares Lifetime ISAs. What’s more, stocks & shares LISAs often have a wide range of investment vehicles, like stocks, ETFs, and funds. Finding a company that offers what you seek is paramount.

Fees are also an essential factor. Checking everything from platform charges and account management fees to account closure and early withdrawal penalties is crucial. High costs can significantly reduce your final savings, reaching and exceeding thousands of pounds in extreme cases.

With these crucial points in mind, let’s explore our recommended providers’ products and fees.

We’ve reviewed the best LISA providers in the UK in detail below. Please note that the information we’ve shared below comes from hours of research. Our team spent days analyzing and assessing each service provider. Since sharing everything we discovered in one guide is impossible, we’ve focused on critical details only. After reading our reviews, please visit each company’s official site to learn more.

1. Skipton Building Society – The Homebuyer’s Safety Net

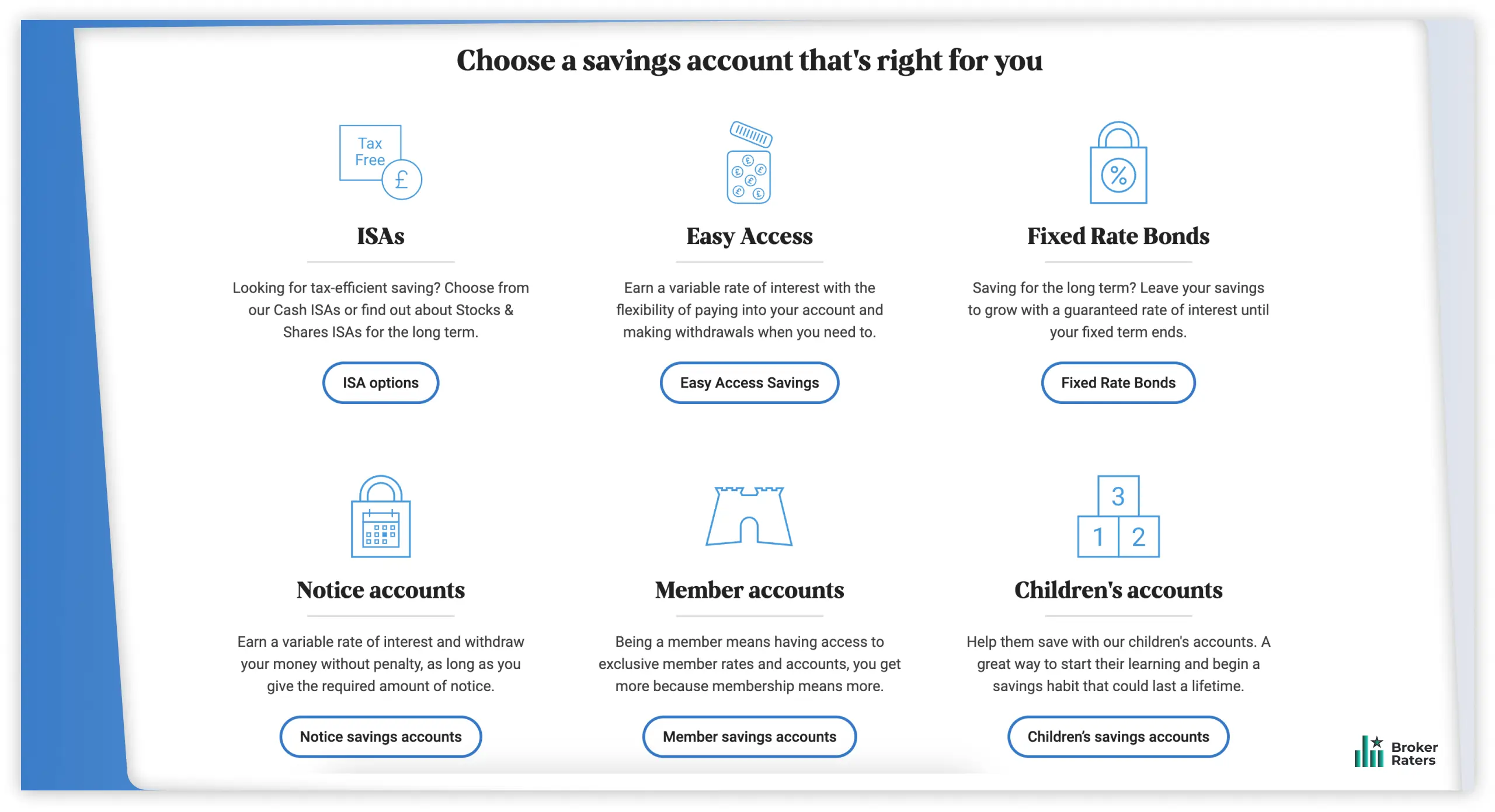

Skipton Building Society offers a cash Lifetime ISA you can use to buy your first home. You can save with this institution and take your first step to affording property worth up to £450,000. And you won’t have to worry if your savings aren’t enough to cover the full cost of your dream property. Skipton Building Society has a variety of variable and fixed mortgages.

While starting out, you can use the Affordability Calculator provided by this Skipton to determine how much you can borrow. Then, when it’s time to buy your first home, this building society’s experts will help you evaluate your desired property for free and advise you on the best mortgages for your unique needs. Taking out a mortgage with Skipton makes you eligible for a £250 cashback reward.

Saving with LISA is rewarding since this service provider has no management or annual fees. Rest assured, accumulating charges won’t erode due to accumulating charges. Plus, Skipton offers competitive yearly interest rates of up to 2.80% tax-free/AER.

Pros & Cons

Pros

Fee-free LISA accounts

Solid reputation acquired over nearly 2 centuries

Offers a variety of fixed and variable mortgages

Free property valuation for first-time homebuyers

Excellent customer service

Low minimum monthly contributions limit

Cons

Only offers CASH Lifetime ISA

Offers variable interest rates that can dip at any time

2. Hargreaves Lansdown – The Investor’s Playground

Are you an avid and savvy investor? Open a Lifetime ISA with Hargreaves Lansdown. You’ll get uncapped access to over 3,000 funds and UK/overseas shares. Additionally, you’ll get the opportunity to invest your money in ETFs, bonds, and investment trusts. The company offers investment hacks and ideas to help you pick the best product.

If you are new to the investment scene but would still like to save with Hargreaves, don’t fret. This company offers ready-made investment portfolios from which you can choose. They come with funds chosen by HL experts and are ideal for people who don’t know where to invest. With a ready-made portfolio, you only need to pick the right fund based on your goals and risk tolerance levels.

You can open an HL Lifetime ISA with a lump sum starting from £100 and top up your account whenever you’re ready. Alternatively, you can set up automated direct debit deposits and invest hassle-free from £25 each month. Any cash held in your Lifetime ISA account will attract interest rates ranging from 2.50/2.53% tax-free/AER to 3.25/3.30% tax-free/AER, depending on your account balance.

Pros & Cons

Pros

Vast selection of investment vehicles

Offers self-directed and ready-made investment options

Excellent interest rates, especially for accounts with high balance

Reliable customer service

Strong reputation built for over 40 years

Cons

Higher fees than its peers

No cash LISA option

3. OneFamily – The Ethical First-Timer’s Choice

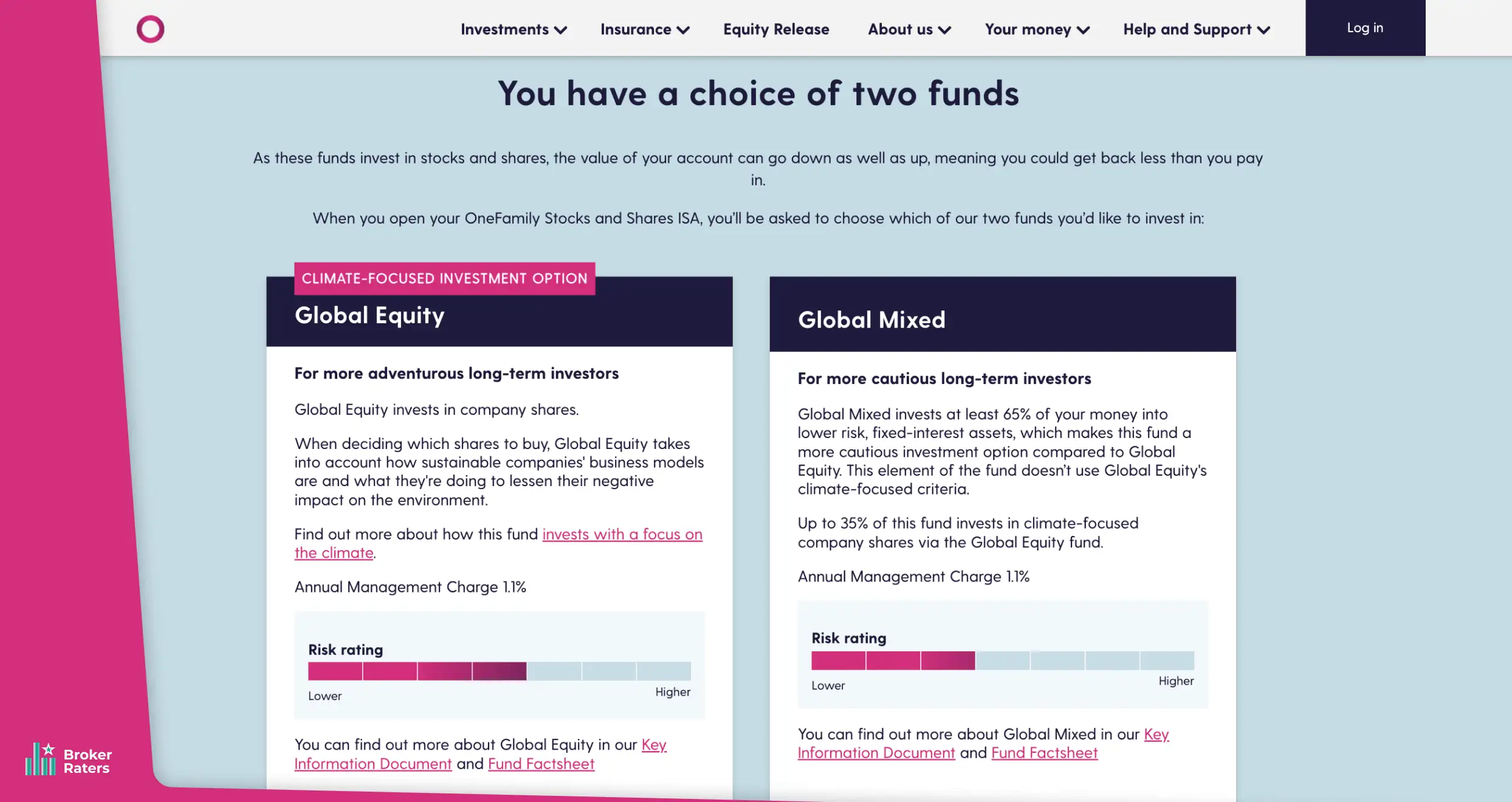

Socially responsible people who are new to saving and investing with LISA should check out OneFamily. This company offers a unique product called Global Equity, which prioritizes investing in shares from companies with the most sustainable business models. Rest assured, your money will be invested in entities that go above and beyond to lessen any negative impact they may have on the environment.

If you find Global Equity’s sustainability-focused criteria too risky, you can opt for its alternative, Global Mixed. The company will invest 65% of your nest egg in assets with lower risk and fixed interest rates. The rest, i.e., 35%, will go to reputable climate-focused company shares. This is the best option for cautious long-term investors who’d still like to play their part in environmental conservation.

Set up a Lifetime ISA with OneFamily with a £250 lump sum or a £25 monthly direct debit, depending on your circumstances. This company has been running for nearly half a decade and has built an unshakeable reputation, so your money will be safe.

Pros & Cons

Pros

Credible, trustworthy company

Sustainable investment options for environmentally-conscious savers

Low-risk investment options for cautious savers

Excellent customer service

Simple, transparent fees

Cons

No cash LISA

Fewer investment options compared to its peers

4. AJ Bell Youinvest – The DIY Investor’s Toolkit

AJ Bell Youinvest’s cost-conscious approach makes it the best option for DIY investors. Open an account with this provider and invest in thousands of funds, ETFs and shares. You’ll also get access to hundreds of investment trusts, gilts, and bonds. You can buy and sell diverse financial instruments with an AJ Bell Youinvest LISA. But note that this activity will expose you to dealing charges of up to £5.00 each time you partake.

As an AJ Bell Youinvest client, you can hold cash in your LISA account for as long as it takes you to find an ideal investment vehicle. Your hard-earned money won’t be subjected to any charges; in fact, it will earn interest and grow over time. What’s more, you can seek professional guidance from the company’s specialist whenever choosing the right investments becomes problematic.

Join AJ Bell Youinvest today and get free access to the popular Shares magazine. It’ll give you unlimited access to invaluable investment information and guidance. If you like what AJ Bell Youinvest offers but are not ready for DIY investing, you can either seek expert assistance or choose a ready-made portfolio for the time being.

Pros & Cons

Pros

Excellent range of investment options

Self-directed and ready-made portfolios

Free expert advise

Simple, beginner-friendly platform interface

Excellent reputation

Cons

Higher platform fees than its peers

No dedicated cash LISA option

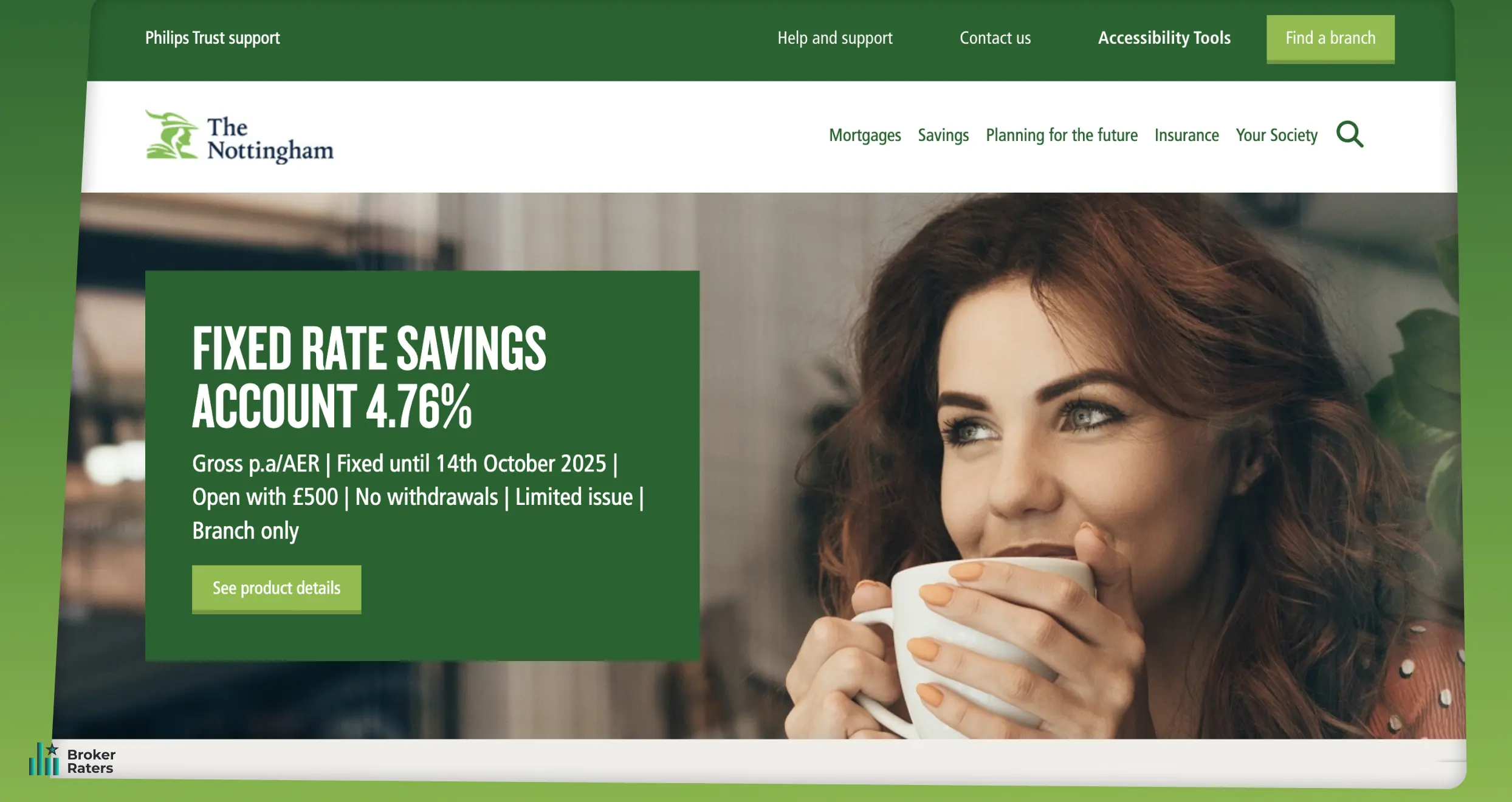

5. Nottingham Building Society – The High-Interest Savings Hub

Nottingham Building Society is one of the UK’s most reputable regional building societies. Founded in 1849, it has faithfully served hundreds of thousands of Brits for nearly two centuries. That is one reason we highly recommend this service provider. Secondly, Nottingham Building Society has juicier interest rates than most of its peers.

Nottingham’s Online Lifetime ISA product currently comes with a 3.00% tax-free p.a./AER interest rate. That is significantly higher than what many of its competitors offer. This service provider has both cash and stocks & shares Lifetime ISA options to make the deal more enticing. These products can help you transition to homeownership or save for retirement.

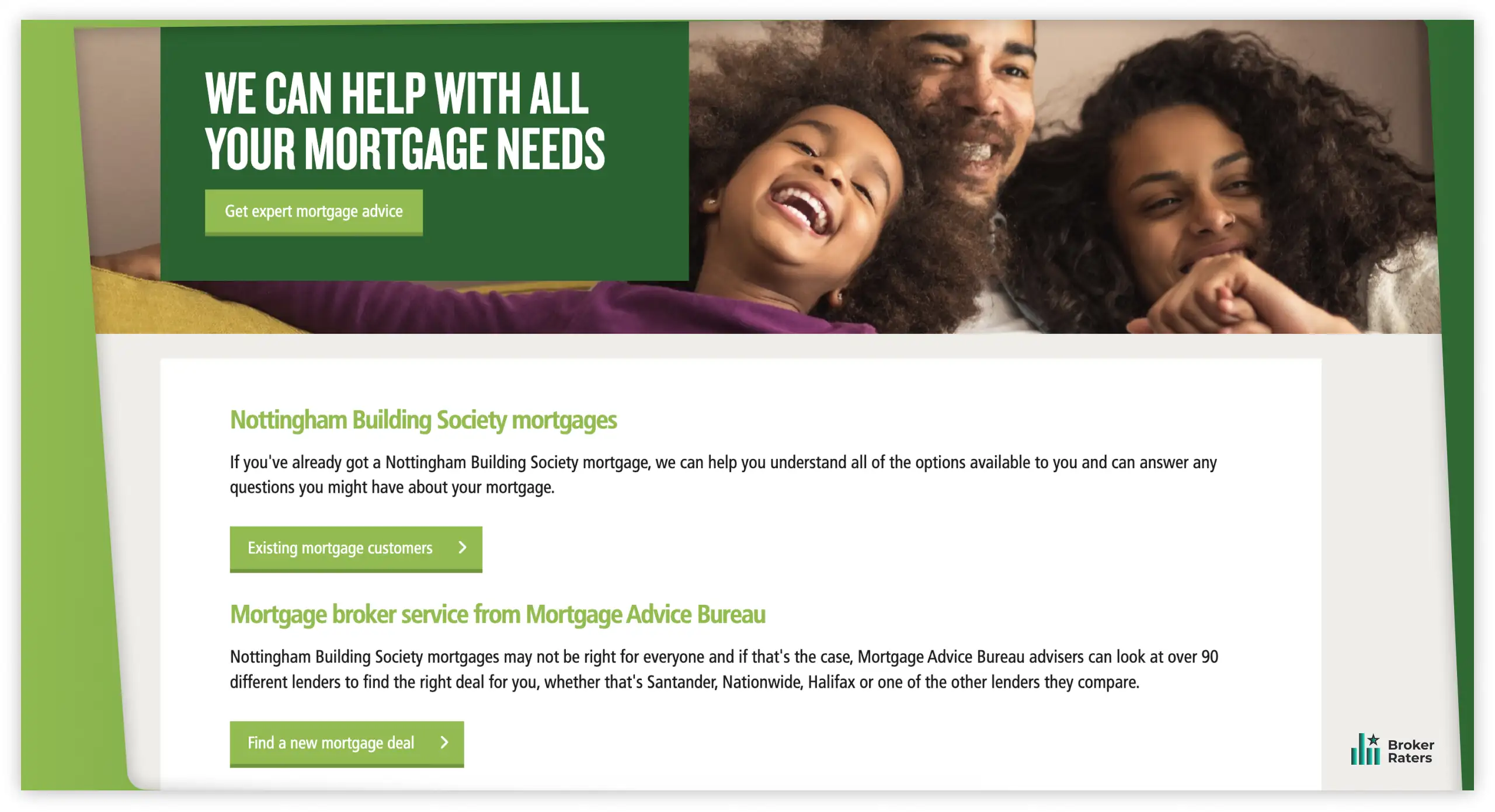

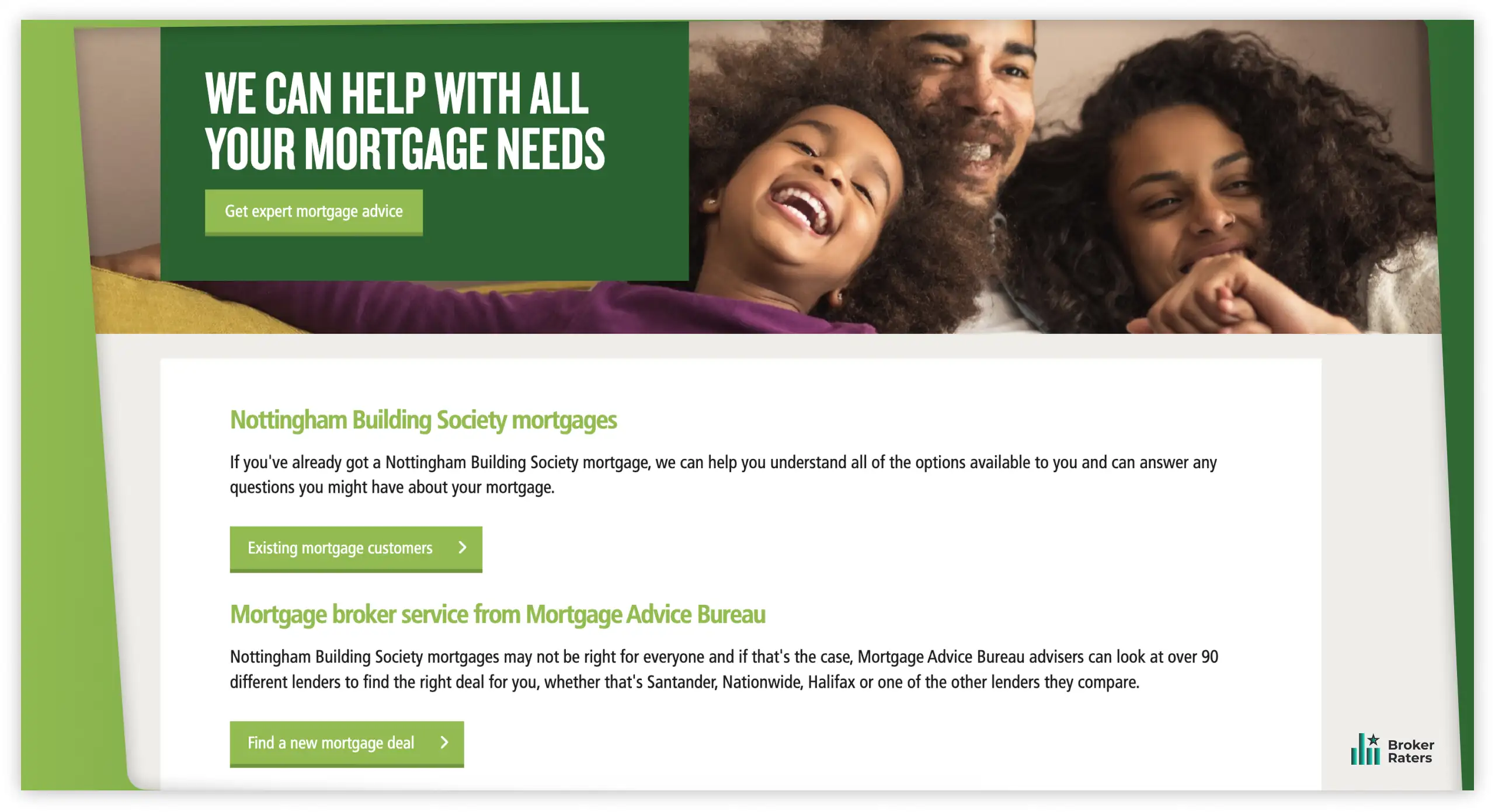

If you choose to use your LISA to purchase your first home, the Nottingham Building Society will help you go all the way with 1,200+ mortgages from 90+ credible lenders. The best part is that you can open an account with this provider with as little as £1.

Pros & Cons

Pros

A trusted provider that’s been around for over 175 years

High interest rates

Offers both cash and shares & stocks Lifetime ISAs

Fewer fees than its peers

Good customer support

Cons

Limited investment products compared to its peers

Scanty research tools for investors

Lifetime ISA – What You Need to Know

Lifetime ISAs are for Brits aged 18 to 39. After opening a limited ISA, the minimum amount you can contribute every month will depend on your chosen service provider. But you can only contribute a maximum of £4,000 per year. Additionally, you can only contribute to your LISA until you turn 50, after which you can’t make contributions or earn the stipulated 25% government bonus.

You can use the funds in your LISA to retire comfortably or purchase your first home. Any Brit planning to fund their retirement with money in a Lifetime ISA can access it once they turn 60. Contravening this rule attracts a 25% withdrawal penalty.

But you can withdraw your money without getting penalized if you have a terminal illness and doctors have given you less than 12 months to live. Furthermore, if your LISA has been active for over 12 months, you can use the money in it to buy your first home without attracting any penalties. But the property you plan to acquire shouldn’t exceed £450,000.

Two types of LISAs are available today: cash and stocks & shares. A cash LISA is like a conventional bank account that lets you save and earn interest. On the other hand, with a stocks & shares LISA, your money is invested in financial assets like stocks, shares, and ETFs. Stocks & shares Lifetime ISAs are riskier since the value of investment products often fluctuates with changing market conditions.

Is LISA Suitable for You?

There’s no denying that a LISA can be an excellent tool for saving for retirement or your first home. That said, whether or not this product is suitable for you depends on numerous factors, including your age and financial goals. LISA can’t be a suitable savings or investment vehicle if you are below or above the 18-39 age cap. You must be within the stipulated age bracket. Moreover, your goals should either be saving for retirement or your first home.

How to Choose the Best LISA Provider in the UK

Tens of providers cater to Brits in the UK. But you should be careful because some of the available service providers don’t offer the best terms and services for your needs. To ensure you hit and exceed your financial goals without facing any major hurdles, use these factors to choose the best Lifetime ISA in the UK provider:

Reputation and Trustworthiness

Offered Products

Interest Rates

Fees and Charges

Customer Service

Always choose a reputable Lifetime ISA provider. Before opening and funding your account, ensure the company is regulated by the FCA and covered by the FSCS. Read customer reviews and testimonials to get a clearer picture of how it measures up in terms of service delivery and customer experience.

Use your financial goals and risk appetite to identify the best LISA investment product, whether a cash LISA or stocks & shares LISA. Then, find a service provider with your preferred investment product. Don’t sign up before checking your chosen provider’s products because, whereas some companies have both cash and stocks & shares LISAs, many only offer one of these options.

Interest rates determine your money’s growth over time and, eventually, the size of your nest egg. The higher the rates, the more your money grows and the bigger the nest egg you’ll have access to at the right time. While vetting each provider’s suitability, consider the stipulated interest rates. Also, check if the offered rates are fixed or variable.

High fees can undermine your ability to save for your first home or retirement with a Lifetime ISA. Before opening up an account, check the service provider’s costs and charges. Examine everything from account management and transaction costs to dealing and exit fees. If your chosen company has fee-free products, good for you. If not, ensure the stipulated charges are reasonable and competitive.

Good customer service is indispensable to both first-time and seasoned Lifetime ISA holders. Excellent support ensures you have the assistance you need to navigate your chosen platform, resolve pertinent issues, and more. Consider every company’s support team’s operating hours and available communication channels. You can also ask a few questions before signing up and gauge the responsiveness, professionalism, and knowledgeability of the service providers’ representatives.

Why Should You Get a Lifetime ISA?

We encourage Brits aged 18-39 to choose credible financial institutions and get a Lifetime ISA as soon as possible for the following reasons:

The UK government tops up contributions to Lifetime ISAs with a 25% bonus

The interest, capital gains, and dividends associated with LISAs are 100% tax-free

Lifetime ISAs are an excellent tool for first-time homebuyers

The funds in a Lifetime ISA can supplement other retirement savings

Brits can start saving in Lifetime ISAs as soon as they turn 18

LISA Pros and Cons

We feel you should know the following pros and cons of the Lifetime ISA before making the final leap and making a long-lasting commitment.

Pros & Cons

Pros

Lifetime ISAs attract a generous government bonus

LISA earnings are tax-exempt

First-time home buyers can make penalty-free withdrawals from LISA funds after 12 months

Terminally ill people can withdraw money from their LISAs without any penalty

LISAs have flexible savings and investment options

LISAs encourage disciplined savings

Cons

Early, non-eligible withdrawals attract a 25% penalty

Limited use of LISA funds

Stocks and shares Lifetime ISAs carry significant risks

Conclusion

The right Lifetime ISA provider can be an indispensable stepping stone to saving for a comfortable retirement or affording your dream home. So choose carefully. We strongly recommend avoiding companies with obvious red flags, such as high fees, uncompetitive interest rates, and a terrible online reputation. When in doubt, consult a seasoned financial advisor before opening a Lifetime ISA with a specific service provider.

Have you been privileged to get trading insider information? But who doesn’t want that unfair advantage? Meet your insider source, Thadeus Geodfrey. He provides insider information on anything trading. But the information he shares is not the kind that would get you in trouble with regulators. Thadeus writes on trade and investment.

With more than a decade of experience, Thadeus has an eagle eye for spotting opportunities and risks. If he tells you a specific broker isn’t to be trusted, you better believe him. He has been swimming in these trading waters long enough to spot scam brokers from afar. Thadeus’s priority is your safety as an investor or trader.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.