Thadeus Geodfrey is an experienced and celebrated writer and self-taught trader specialising in cryptocurrencies and forex. Market analysis, identifying fraudulent brokers, and security are his cup of tea. At BrokerRaters Thadeus develops educational materials and user guides, offers market insights, and ensures our content conforms to the best standards. Join Thadeus to succeed in your trading endeavors.

Fact checked

Advertising Disclosure

We may receive compensation from our partners for placement of their products or services, which helps to maintain our site. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn’t influence our assessment of those products.

A Cash ISA offers tax-free interest and a safe haven for your hard-earned money. Board this financial vehicle towards the world of flexibility, high interest rates, fixed returns, and innovative saving approaches. Moreover, the government-backed security plus tax-free returns give you peace of mind and help you focus on growing your wealth without worrying about losing even a penny.

But navigating the crowded Cash ISAs market is akin to hunting for a needle in a haystack–thanks to the countless options, varying fees, and fluctuating interest rates. The good news? We have done the legwork for you! Our experts rounded up the top five best cash ISA platforms in the UK based on their minimum monthly contributions, licensing, and annual interest rates. You’ll also discover their products, pros and cons, and how to choose the right one.

First in our guide is a quick comparison table of the ISA platforms. Its main objective is to give you an overview of what these institutions offer so you can decide if they meet your expectations as early as possible. In the table, we’ve highlighted the most important factors, i.e., regulatory status, minimum monthly contributions, and annual interest rates.

Please note that the information on the table doesn’t cover everything. After perusing this and the other tables in this guide, read each institution’s review for more information.

We’ve also included separate comparison tables for products and fees below. Our objective, as always, is to help you find a service provider that aligns with your needs, goals, and expectations. The important thing to note is institutions have different products and fees. Be careful, lest you choose a provider that either lacks your preferred financial products or charges exorbitant fees.

We now bring you a deeper look into these top-choice providers. Our review will help you settle for one that caters to your savings goals and needs. However, we encourage you to visit their official websites to catch any updates and see whether it suits you. Remember to scour review sites, too.

1. Barclays – Best for Tech-Savvy Savers

If you’re a tech-savvy Cash ISA saver, you probably desire a mixture of online, app, and telephone banking. Barclays is among the best Cash ISA UK Providers, allowing you to enjoy these services as long as you’re a registered account holder.

Our research and tests confirmed that the provider’s various Cash ISA options have flexible and competitive interest rates. Looking to enjoy liquidity and anytime access to your funds? We recommend their Instant Cash ISA. This option provides a 1.66% AER for balances up to £10,000 (the rate will adjust to 1.51% AER from December 2024). For higher amounts, you get 1.21% AER.

Those who desire higher returns opt for Barclay’s fixed-rate Flexible Cash ISAs. The interest rates are 3.90% AER and 3.60% AER for the 1-year and 18-month packages, respectively. And the icing on the cake? Enjoy up to three penalty-free withdrawals for both of them, each limited to 10% of the balance. Furthermore, you can transfer funds from an existing ISA account to your normal one or another ISA.

Perhaps you desire exclusive accounts to meet your significant savings or wealth management needs. You can choose their Premier 1-Year Flexible Cash ISA or Wealth 1-Year Flexible Cash ISA, which provides a 3.95% AER. Their 18-month counterparts’ interest rate is 3.65% AER.

Pros & Cons

Pros

Wide range of Cash ISAs, including Instant, Fixed-Term, Premier, and Wealth

Competitive fixed rates if you desire guaranteed returns

Fixed-term ISAs provide some liquidity

Smaller savers enjoy banded rates on Instant ISAs

Charge-free transfers if you want to consolidate savings

Cons

Larger balances in Instant ISAs have low rates

Only specific customers enjoy higher rates and exclusivity

2. HSBC – Best Cash ISA UK Provider for Flexible Access

If you’re like most UK investors, flexible accessibility is your dream. Usher in HSBC to enjoy various tax-free savings solutions and attractive interest.

Their Fixed Rate Cash ISA offers a fixed rate of 4.05% AER for a 13-month period, which means you can predict your returns. While you need to deposit a minimum of £500, you can transfer from other ISAs to consolidate the amounts. Furthermore, the account transitions to a Loyalty ISA at the end of the term without charges or restrictions on cash access.

Earn for staying loyal to HSBC. We recommend the provider’s Loyalty Cash ISA for its generous “thank you” gesture–each deposit gets a loyalty interest rate for one year. The figures are 3.20% AER for HSBC Premier account holders and 2.70% AER for other accounts. After this period, you get 2.30% AER until you make another deposit.

One unique standout is HSBC’s Stocks and Shares ISA for those looking to invest and save their returns away from the sneaky capital gains tax. You can cherry-pick from ready-made portfolios or various funds and shares. A minimum of £50 is all you need to kick-start your journey, as long as you’re a UK resident aged 18 and haven’t exceeded your annual ISA limit. You can easily access funds from sold investments within four business days.

Pros & Cons

Pros

Flexible ISAs, including Cash, Loyalty Cash, and Stocks & Shares

Minimum investment of $50 in Stocks & Shares ISA offers flexible accessibility to beginners

Access to global investment opportunities

User-friendly mobile app and online platform

Easy transfers from other ISAs, enabling savings consolidation while retaining tax benefits

Market and investment risks may cause losses in Stocks & Shares ISAs

3. Lloyds Bank – Best for Classic, Simple Saving

Simplicity is at the core of Lloyd Bank’s ISAs. Whether you desire steady growth with fixed rates or flexible access to your funds, the provider has an option for you.

Its 1-Year Fixed Rate Cash ISA is a haven of certainty. Enjoy 3.80% AER for over 12 months after depositing a minimum of £3,000. Moreover, you get an extra 0.10% if you stay a loyal current account holder. Your ISA automatically transitions to an Instant Cash ISA afterward.

Want to lock in your savings for a longer period? Sign up for their 2-Year Fixed Rate Cash ISA and get a solid 3.40% AER plus the same loyalty bonus. While you still need to make a minimum deposit of £3,000, you enjoy guaranteed returns.

The huge minimum deposits shouldn’t scare you if you are a small saver–Club Lloyds Advantage ISA Saver welcomes you with only a £1 minimum deposit requirement. Furthermore, its enticing 3.80% AER for up to three withdrawals annually helps you access your funds without sacrificing growth. Note that the rate drops to 1.20% AER for more withdrawals. What a way to encourage discipline!

Another option for small savings is the Cash ISA Saver. It accepts a minimum deposit of £1 and has tiered interest rates: 1.30% AER (on balances less than £25,000) to 1.80% AER (on balances exceeding £100,000).

Pros & Cons

Pros

Diverse options to meet short and long-term savings needs

Competitive interest rates as high as 3.80% AER

Loyalty bonus of 0.10%

Low minimum deposits on some ISAs

Flexible access to up to 3 penalty-free withdrawals on some accounts

Cons

Fixed Rate ISAs limited to up to just 2 years

Fees on early withdrawals discourage early liquidity

4. Nationwide Building Society – Best for Newbie-Friendly Options

Our researchers discovered two beginner-friendly ISA options in the Nationwide Building Society, one of the best Cash ISA providers in the UK. Plus, this treasure trove’s interest rates are among the most competitive in the industry.

Are you hunting for a savings pot with occasional access plus competitive returns? Let’s introduce you to the provider’s 1-Year Triple Access Online ISA. This tier gives you a 4.10% AER as long as you stay within three withdrawals yearly. Exceeding this limit pushes the rate down to 2.00% AER for the term’s remainder. You can easily access your withdrawals by transferring funds to Nationwide Current or a suitable instant access account.

Stability seekers will love Nationwide’s 1-Year Fixed Rate Cash ISA. It locks in a 4.10% AER, allowing you to save that lump sum you won’t need for the next year. In our view, it’s among the best Cash ISA rates in the UK. While early withdrawals close the account and incur charges, we find this a great way of encouraging growth.

You can trust Nationwide Building Society to keep your savings under lock and key. Their FSCS protection covers up to £85,000 deposits. Furthermore, the provider welcomes you into its membership society for more benefits.

Pros & Cons

Pros

Flexible options, including triple access and fixed rate

Competitive interest rates of up to 4.10% AER

Secures up to £85,000 under FSCS

Easy access in-app, in-branch, or online access

Flexible transfer of funds across ISAs without losing tax benefits

Cons

Early withdrawing from fixed-rate ISAs closes the account

The attractive introductory rates decrease if you don’t stay vigilant about the terms

The 1-year period might be less for long-term enthusiasts

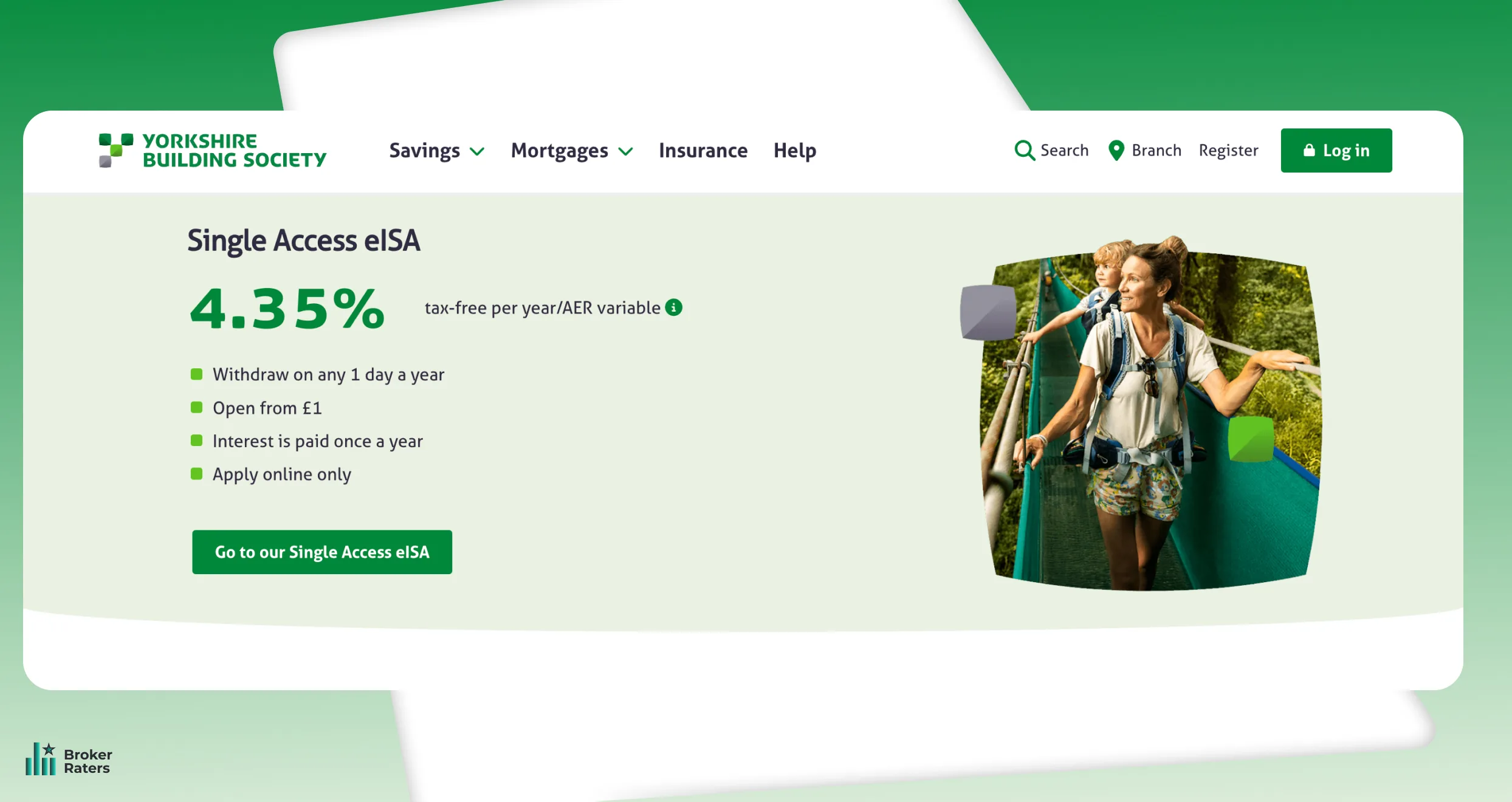

5. Yorkshire Building Society – Best Fixed Rate ISA UK Provider

Yorkshire Building Society is, according to our findings, the best fixed rate ISA UK provider. A £100 minimum deposit ushers you into the Fixed Rate Cash ISA (until 31 December 2025), which currently offers a 3.90% AER.

You can also choose a higher-term eISA option that locks savings at the same interest rate until January 2028. Alternatively, they have an option that extends the period until December 2029, although the interest drops to 3.50% AER. Just beware that early account closure attracts interest penalties ranging from 90 to 360 days.

YBS also has something for those looking for high liquidity, low deposit requirements, and competitive returns: Easy Access ISA Issue 2. Grab its 4.30% tax-free AER and penalty-free withdrawals at any time. The minimum deposit amount to open an account is £1.

The provider allows only online access to these ISAs to promote easy management. Furthermore, FSCS safeguards up to $85,000 of your savings.

Pros & Cons

Pros

ISA options tailored to your needs, including fixed-rate and easy-access

Low opening balance, starting from £1

Attractive interest rates of up to %4.30 AER

User-friendly online account opening and management

Greater liquidity due to penalty-free Easy Access ISAs

Cons

Limited ISA types and lacks stocks and shares, lifetime, or innovative finance ISA.

Early withdrawal from Fixed Rate ISAs attracts interest loss

Cash ISAs – What You Need to Know

You can’t wait to start saving without the taxman demanding a cut of your interest earnings. But before grabbing an ISA account, our experts have a few pointers that will help you get the best out of your savings:

Tax-free saving

The tax-free interest earnings are behind Cash ISAs’ popularity. You can now bid farewell to those taxes on interest gotten from standard savings accounts, allowing you to boost your returns.

Using the ISA allowance

Your ISAs can only hold up to a set amount each tax year (£20,000 in 2024/25). The amount will be reset on April 5, and the unused allowance will not be rolled over to the next year. That means you permanently lose the ability to save that amount tax-free.

Transferring ISAs

Are you frustrated with low-rate ISA? You can transfer it to a better-paying provider. But we recommend you use the provider’s transfer process rather than withdrawing and re-depositing the money. This route helps retain your ISA’s tax-free status and stay within regulations. The transfer period is typically up to 15 business days.

Flexible cash ISAs

With flexible ISAs, you can withdraw and replace funds within the same tax year without reducing your annual allowance. But this benefit doesn’t apply to all ISAs.

Lifetime tax-free benefits

Your Cash ISA’s savings can stay tax-free in the account year after year. So, why don’t you use the annual allowance to build substantial, tax-free balances over time?

Safety of savings

ISA-held funds enjoy up to £85,000 per provider under FSCS. Thus, you can rest assured your savings won’t vanish into thin air.

Opening multiple ISAs

You can now open and contribute to multiple Cash ISAs during the same tax year. For example, you can have a Fiex Rate and Easy Access Account. Just remember that your total deposits can’t exceed the £20,000 allowance.

Consolidating ISAs

While you can open several ISAs, we recommend consolidating them into a single account. This trick simplifies management and often boosts the overall interest rate. But remember, amounts above $85,000 may not be FSCS-covered.

Are ISAs Suitable for You?

Given increasing interest rates and shifting tax implications on savings in the country, an ISA might be the right route. But how can you decide if it’s the route to take?

Since 2016, Personal Savings Allowance (PSA) has allowed people to earn tax-free interest on savings up to specific thresholds based on their tax-rate brackets. Basic-rate (20%) and higher-rate (40%) taxpayers can earn up to £1,000 and £500, respectively, while additional-rate taxpayers don’t get any PSA.

Few savers surpassed these allowances between 2016 and 2022 due to low rates. However, the recent rate hikes mean you need significantly lower savings to hit the PSA cap–£20,000 and £10,000 for basic-rate and higher-rate taxpayers, respectively. Previously, the former needed as much as £250k to generate taxable interest, showing how much the landscape has changed.

So, who benefits most from ISAs? Moving funds to a Cash ISA can shield your earnings from taxation if you fall under one of the following:

Already paying tax on savings interest

Nearing the PSA limit

Require the more long-term flexibility fixed-rate Cash ISAs offer over fixed-term savings accounts.

How to Choose the Best Cash ISA in the UK

Cash ISA platforms in the UK offer an attractive interest rate, flexible access, easy management, and other advantages. Let’s take a deeper dive:

Interest Rate

Access Flexibility

Minimum Deposit

FSCS Protection

Penalties and Charges

Interest rates often vary across Cash ISA types and providers. You may go with fixed-rate ISAs for consistent interest and set periods. Usually, higher-rate accounts require locking your funds in for longer periods.

Instant access ISAs are suitable for short-term needs because you enjoy penalty-free withdrawals. On the contrary, early withdrawals in fixed-term accounts attract charges. ISA accounts labeled “flexible” allow you to replace withdrawn funds without affecting your annual allowance.

Some providers allow you to kickstart your ISA account with just £1. We recommend them for drive testing or if you’re a small-scale beginner. Regular saver ISAs have juicier rates if you contribute monthly without failure.

Your provider should have FSCS coverage for your funds. However, once you exceed the £85,000 limit, remember to obtain coverage for additional amounts.

Most savers overlook this crucial factor. Look into a provider’s penalties, such as reduced interest rates after several withdrawals in a year or account closure. That way, you can manage or evade such charges without surprises.

Why Should You Get a Cash ISA?

A Cash ISA is a wonderful vehicle for reaching your savings goals and helping you meet diverse financial needs. Consider boarding one because of its benefits.

First, it offers tax-free interest, unlike regular savings accounts, which require tax payments once you exceed PSA. It also helps protect savings from future tax, especially now that hitting the PSA threshold is becoming increasingly easy.

You can also harvest higher returns over time and oscillate across different ISA options. Furthermore, these vehicles enjoy government-backed protection in the form of FSCA cover.

Other attractive reasons include future savings, flexibility, and temporal accessibility. With Flexible Cash ISAs, you can withdraw and replace money within the same tax year while keeping the annual allowance intact.

Pros and Cons

It’s time to weigh Cash ISAs’ strong areas vs drawbacks. Here we go:

Pros

Tax-free interest

Protection from tax hikes

Various options and types to suit your financial goals

You can enjoy the best Cash ISA rates in the UK

FSCS-backed cover for up to £85,000 of your savings per provider

Up to £20,000 annual ISA allowance encourages long-term tax-free savings

Cons

Often lower interest rates than standard savings accounts

The ISA allowance may not be enough for savers with large sums

Fixed-rate ISAs can slap you with early withdrawal penalties

Lower growth potential than stocks and savings ISAs

Inflexibility in some accounts can tie up your money during an urgent need

Conclusion

Cash ISAs are an excellent way to catapult your savings while enjoying tax-free benefits. But you need to play your cards like a pro.

Our experts advise you to choose providers that fit your financial goals and needs, such as flexible terms, competitive rates, and adequate protections. Remember to check their fees, penalties, and restrictions on transfers and withdrawals. Furthermore, always read the fine print and stay vigilant about introductory rates and evolving terms.

The right place to start is the providers’ comparison tables, which compare their different ISA options. Next, review expert opinions and online reviews before settling with your best Cash ISA provider in the UK.

Have you been privileged to get trading insider information? But who doesn’t want that unfair advantage? Meet your insider source, Thadeus Geodfrey. He provides insider information on anything trading. But the information he shares is not the kind that would get you in trouble with regulators. Thadeus writes on trade and investment.

With more than a decade of experience, Thadeus has an eagle eye for spotting opportunities and risks. If he tells you a specific broker isn’t to be trusted, you better believe him. He has been swimming in these trading waters long enough to spot scam brokers from afar. Thadeus’s priority is your safety as an investor or trader.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.